Good Morning!

Good Morning!

It's another muggy morning in our part of the world. I know many of you have sent messages with details of too much rain and warm temperatures creating a greenhouse effect in your area. In Central Illinois, we can't seem to buy a rain. While we've had a pop-up shower here and there, it's been few and far between. At this point, my main hope is that we can get a shower before pollination and the heat subsides. This past weekend, we finally broke the 80-degree mark after several days of 95-degree heat. On the black ground, the corn has really grown, while the lighter dirt is showing some stress. I've heard from a few of you sharing your own kidney stone stories; it's certainly not fun. I appreciate those who have reached out with your stories or checking on me. In all honesty, it's quite a deal getting one of those out when they have to work on you to do so. I'm not going to give too many details here, but the last week wasn't the most fun I've had-I'll just leave it at that. I hope your weather stays as you'd prefer. For those who keep getting the rain, I'd appreciate it if you'd spread the wealth. We'd be glad to get just one of those soakers. Keep in touch.

I've spoken with several of you who are trying out the AgMarket app. Since you can get it through the CR program starting August 1, I want to make sure you know we'll have you on a free demo until then if you want to start using it. Given how tight margins are right now, our tool for honing in on break-evens and profitability is as important as ever. Keep your questions coming. CLICK HERE for more info on the AgMarket app. https://hubs.li/Q03qt2Qd0

The corn and bean markets both lost ground on the week. While Friday saw nice gains, particularly for corn, the losses earlier in the week were plenty strong. Very little has sparked buying interest in either market, even as the Eastern Corn Belt has been as hot and dry as it gets. The USDA-planted acreage and quarterly stocks report is out this morning. This is a big one, and for those who are using the app, be sure to listen to the post-market report we'll record after Monday's close. Outside markets were active with mixed signals.

- August crude settled .28 higher on Friday at 93-down 8.41 on the week

- The Dollar settled up .269 at 28, down 1.094 for the week

- The DOW was up 407 on Friday, settling at 44,125-up 1,651 for the week

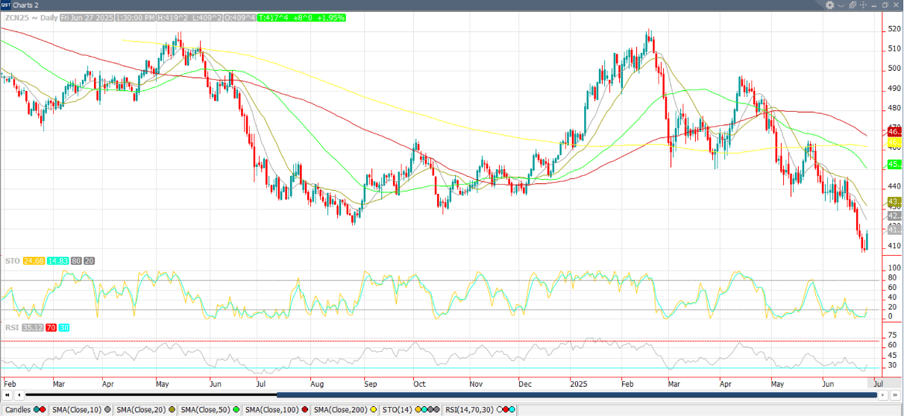

July corn had another tough week, with the death spiral taking a momentary pause on Friday. July settled at $4.17 ½, up 8. This was 1 ¾ off the high and 8 ¼ off the low. July lost 11 ¼ cents for the week. On a week that started with a % drop in crop ratings and as solid demand as we’ve seen, the sellers were as active as ever. I know it’s frustrating for those of you who have been sitting on old or new corn that needs to be sold, but these markets don’t always have to make sense. A significant issue we’ve dealt with over the last few weeks is the sheer size of the Safrinha crop in Brazil. With some reporting yields 14 Bu./A. larger than their biggest crop ever, you can imagine why the trade has been more of a seller of corn. For this Monday report, my AgMarket team came up with an acreage number of 95.8 for corn, so we’ll see how close we are. For planting intentions, the USDA reported 95.3, so yes, my team thinks we’re up overall on the year, even with some acres likely lost in Ohio through the Delta. For stocks, I feel confident the usage of corn has been strong in the first three quarters of the marketing year, and we’ve got to hope we don’t get a surprise there. Given the high demand, the only reason we’d see more corn sitting around is if the USDA underestimated last year’s crop—and yes, it has happened before. Let’s hope we finally get some good news or at least some rebound on these markets.

DEMAND

Corn demand was steady/lower on the week. Net export sales came in at 741 KMT, which was down 150k from a week ago. New-crop sales were 301k, so overall sales were steady. Ethanol grind was at 105 MB, down 3 million bushels, but still a strong number. Stocks were up on the week. Basis is steady:

- My local basis: 18 under July (no change)

- Decatur: 11 over July (no change)

- Louis River: 24 over July (a penny improved)

CASH CORN

Cash prices were, you guessed it, lower on the week. While some areas are seeing a big push for basis, steadying price levels, most areas have seen a slow leak on cash bids. I’ve heard of some $5 corn being paid in Indiana into Ohio as that eastern market continues to try to pull corn out there. It will be interesting to see how this market responds as we approach pollination. While you’d expect the weather to impact new corn more than old, there is no doubt buyers pay attention, especially as they run tight on cash ownership. If we happen to get plenty of moisture across the Corn Belt moving forward, there won’t be much push for old corn, especially with these warm temperatures that will likely bring harvest a bit early this year. On the flip side, if there are questions about the size of this crop coming down, you could see a scramble in those areas tight on corn. It all boils down to the next three to four weeks. If we don’t have a story by then, this cash game will be essentially over. For those with gambling bushels, it seems like we’re all in, so a guy may consider seeing what Mother Nature deals us in the next couple of weeks. It’s personal preference, but regardless, I’d consider having a plan in place in the event we finally get a bounce. My advice remains to keep your offers current.

2025 CORN

December 2025 corn ended the week at $4.27, down 14 ¼. This past week wasn’t a good one at all for the new crop. While the weather was showing plenty of heat, enough areas received the moisture needed to make the heat a non-event. What really smoked the corn market was the continued revisions higher on the Brazilian corn crop. While we have good demand for corn right now, the big concern is that Brazil has significantly more corn to export than it did a year ago, which means US exports are likely to take a hit. How much might the USDA eventually have to trim from US exports? Some think it could be up to 300-400 mb. So the issue is, if we trim our old crop balance sheet again in July to 1.3 bbu or below, the new crop balance sheet could slip to 1.7 bbu or below. If we have to add in a loss of export business of 300-400 mb, we’re right back to 2 bbu of corn. I’m not bearish down here, but we need Mother Nature to at least throw us something to get excited about. It makes no sense to sell at levels you can’t make work, so I’m doing my best to stay patient while we sort out just how big this crop might get. As always, if you’re profitable, I could see making some sales; however, if not, you may need to play the storage game more aggressively than in the past if we can’t rally by harvest. Let us know if we can help you manage some of your risk. Using the AgMarket app or something similar can take a ton of guesswork out of your risk management.

Corn Market Theme: The corn market is testing my patience, but we’ll know more about potential price action after Monday’s report. Keeping flexibility with offers in place above the market is a wise strategy, in my opinion.

July 2025 Corn Chart

BEANS

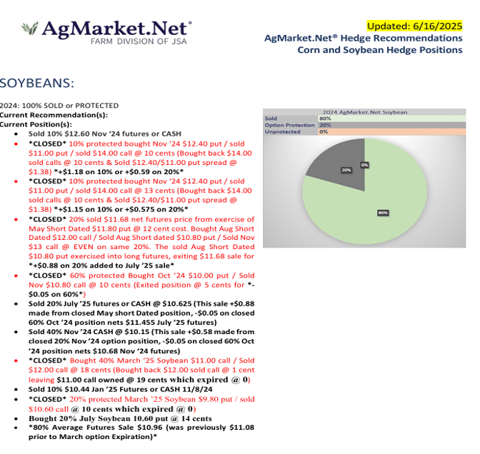

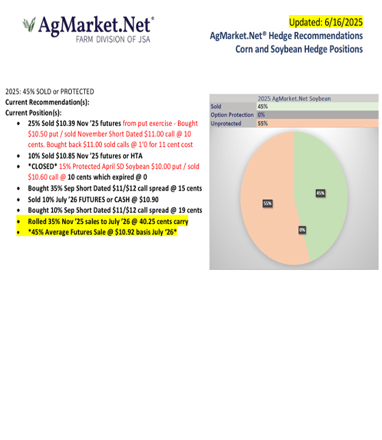

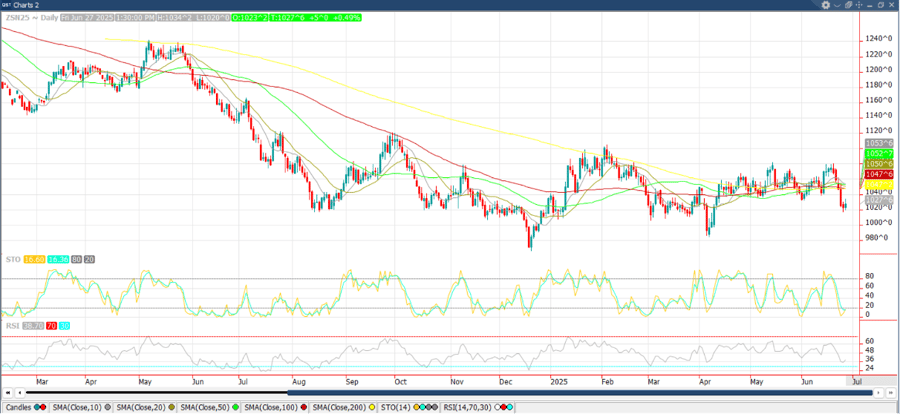

Beans stunk it up this past week with sellers active. July closed at $10.27 ¾, up 5 on Friday. This was 7 ½ off the high and 7 ¾ off the low. Beans were down 40 ¼ on the week. Meal settled 13 lower on the week at 271.1, while soy oil ended the week at 52.45, down 2.02. With this bean market, we have seen some resilient price action for several weeks, up until this past week. Sellers got active, mostly as we saw the crude oil market fall sharply, which spilled over to bean oil. Considering the bean oil rally was a bit part of the bean rally, it’s easy to see why we’d see beans sell-off after bean oil trade $2 lower on the week. For the report, our AgM team came up with an estimate of 83.2 for bean acres; this compares to 83.5 from the USDA in March. Our talks with growers seemed to center on those who went heavy corn and switched some acres directly from beans. On the flip side, where it was excessively wet this spring in the east and southeast, we heard from growers who switched from corn to beans due to how late it got. Our research leads us to believe there were more acres switched to corn from beans. What would really be nice on Monday is a bean rally due to a bullish report, and don’t rule it out. With big demand a well-known fact, some questions on bean production is just what this market needs. As with corn, we’ll know more after the report, but for now, I’d be of the opinion we wait and see how this weather unfolds as well.

DEMAND

Soybean exports were off from last week but still good for this time of year at 403k tons, 100k lower than last week. With 156k posted for the next marketing year, bean exports overall weren’t down much. Basis was steady/wider.

- My local beans: 30 under July (no change)

- Decatur: 20 over November (no change)

- River: 17 over July (4 cents improved)

CASH BEANS

Cash beans were down sharply on the week. While some areas were pushing for beans, it wasn’t near enough to counter the huge drop on the board. It was easily the worst week of trading we’ve seen in some time, so a rebound is sorely needed. Where that may come from remains to be seen, but we’re down to a couple of possibilities, in my opinion. If we can get a lower acreage number, it could precipitate some renewed buying interest, while we have quite a bit of weather to see before feeling good about US bean yields. The tricky thing is Brazil is your biggest bean producer at this point, while the US is easily the biggest corn producer. I realize most of you are down to gambling bushels if you have any at all. This makes it a little easier to be patient. However, if you have many beans at all, we have to remember that the Delta will start harvesting beans in August, which will satisfy the export pipeline and could make it tough to see cash prices rally. Long story short, we’re running out of time to sell beans, so keeping offers current would be wise.

2025 BEANS

November 2025 beans settled at $10.24 ¾, a loss of 36 cents on the week. November beans didn’t have nearly as bad of a week as the old crop contracts. The rough thing about November beans back down here is we’re all looking at sub-$10 prices for fall delivery again. Given that most growers breakeven points are in that $10.50-$11.00 cash area, it’s tough to sell them here. Now, that doesn’t mean they can go down another dollar. I’m not that bearish right now, but Lord forbid we see more bean acres on this report. While it’s a big rally, I’m still of the opinion that, at this point, I wouldn’t want to sell more beans unless I could call it a profit. I’d want to be back over $10.50 at the very least while keeping my sights set on a rally back to $10.85 to $11 basis the board. While a week like last week takes the wind out of our sails and likely makes us not think a rally like this is possible, I’ve seen this bean market rally like gangbusters at times when we didn’t think it was possible. Keep some offers in place and stay flexible as this great weather we’re seeing isn’t guaranteed to continue through the end of August.

Bean Market Theme: As with corn, we will know more after the report about what price action might look like. I’d like to think we have another rally or two in this market, but we need some help from Mother Nature.

July 2025 Soybean Chart

As always, use the AgMarket.Net Profitability App to help you figure out your breakevens and put your plan in place.

Let me know if I can help in any way. These markets are tricky, but with a plan in place, we can take the emotion out and make better decisions.

Matt Bennett

mbennett@agmarket.net

Work: 815-665-0462

Twitter: @chief321