Good Morning!

Good Morning!

I hope your week has gone well and you have a good weekend planned. For some, harvest is getting started, although around home, it’s just a couple of folks. We planted in April, but most of that was beans, so our corn isn’t quite ready. ADM Decatur is taking corn with no drying charge and shrink only, but it must be 25% or less. While our earliest corn looks close, I’m not sure we’re quite there yet. Our April beans that are early Group 3s will likely be the first thing we harvest, and that’s going to be this coming week in all likelihood.

Our fall baseball schedule is almost over already, so I’ll have Toby, the 13-year-old, ready to run a grain cart. Our two youngest are home-schooled, which comes in real handy when we’re in harvest mode. While we keep Toby’s hours in check, he wants to be out there, and he’s as good a help as I can hire, so it’s a big-time blessing to have him running a cart. I appreciate the feedback you all have been giving me. Keep it coming as you get started with harvest; I’d love to hear how yields are running.

My summer speaking tour will wrap up on Monday when I go to Iowa for a Beck’s special event. After that, the next time out will be post-harvest. For those using the AgMarket app, keep the questions and comments coming. HERE is the link for more info on the AgMarket app. https://hubs.li/Q03qt2Qd0

The corn market made a run at closing higher on the week but faltered late on Friday’s session, while beans had a rough week. With plenty of talk of a lack of export demand for beans amid trade/tariff wars, the market seems reluctant to buy beans on a dry finish to the 2025 crop. Outside markets were trading as follows compared to a week ago, late in the trade on Friday.

- The US Dollar was down .01 at 97.725.

- October crude oil was down 1.96 at 62.02.

- The DOW was down 164 points at 45,441.

CORN

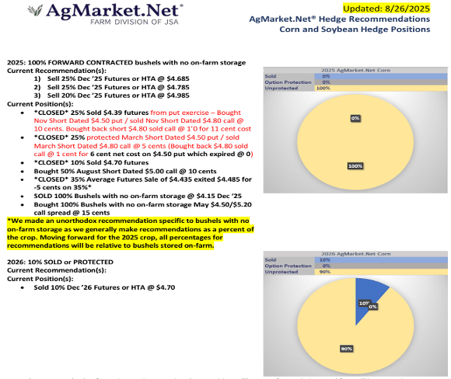

December 2025 corn held together but saw some selling at the close of the holiday-shortened week. On Friday, December settled at $4.18, down 1 ¾. This was 4 ¾ off the high and 1 ¼ off the low. December lost 2 ¼ cents for the week. With the corn market hearing everything from the crop is as good as the USDA August number to some talking about a struggle to get to 180, we’ve had several different ideas on market direction. Yes, this is a big crop; no one is disputing that. However, disease pressure has taken a chunk off some of the lofty Iowa yields while a dry finish has certainly impacted much of the ECB. Demand remains strong for corn, particularly in the ethanol and export sectors. While we aren’t getting cattle from Mexico come north of the border due to the New World Screwworm, we’re shipping corn to them to feed those cattle. I assume with a yield drop this coming Friday, the USDA could stand to shave a fair amount of the new-crop feed usage. Either way, it will be tough to chew the stock numbers much below 2 bbu just yet. On the bright side, we have a ton of demand to fulfill with a grower that isn’t impressed with fertilizer prices here at pre-pay time. I remain of the opinion corn has a shot at being something a guy wants to have ownership of on down the road, but it may take some patience.

DEMAND

Corn demand continues at a strong pace with cancellations of old-crop and big new-crop sales. Net export sales came in at -281 KMT, which was 260k more in cancellations than a week ago. New-crop sales were again impressive at 2.117 mmt. Overall sales were quite similar to a week ago. Ethanol grind rose a bit to over 104 MB. Stocks were a tic higher on the week. Basis was widening:

- My local basis: 42 under December (widened 7 cents)

- Decatur: 15 under December (no change)

- Louis River: 8 under December (no change)

CASH CORN

Cash prices weren’t doing much on the week. With the small drop on the board and basis steady to wider, most bids were off from a week ago, but not by much. Growers seem reluctant to sell any corn as harvest gets underway. Given the dry finish to the crop, many are assuming the USDA will have to ratchet down yields, and prices could rally as they did a year ago. While that’s certainly a possibility, I wouldn’t get too hopped up on a big rally anytime soon unless the USDA really slashes corn yields. While many feel they should, it’s not typical for the USDA to make big changes on any report, so getting to their final number may take a couple of good whacks at yield. We also must remember that several of the surveys are still showing the grower thinks the crop is closer to USDA’s 188.8 than ProFarmer’s 182.7. I think we’re in that low to mid-180s, but I could certainly be wrong. Every year is different, but it would be tough to assume we didn’t do some damage with one of the driest Augusts we’ve seen over a bulk of the corn-belt in the last 100 years. I’d be willing to reward rallies if you can make these prices work, but I’d also keep some ownership.

2026 CORN

December 2026 corn ended the week at $4.58 ¾, down ½. This 2026 corn sure looks to me like a market that could hold some value for the time being. Given high input costs, one can’t help but assume drastically lower corn plantings this coming year. Given that many growers are corn to beans and vice-versa, we should see the high fertilizer prices impact both conventional corn acres and corn-on-corn acres alike. As with old crop, I’d keep some flex in the plan, but I’d also be ready to lock in some stronger levels, should we see those unfold. Long story short, we’ll have plenty of old-crop bushels most likely, while seeing a real need for corn to rally to hold onto enough acres to satisfy demand in 2026. The only caveat is if bean prices would get clipped. That’s certainly possible, but given the dry finish, bean values shouldn’t fall out of bed completely.

December ’25 Corn Chart

Corn Market Theme:

The corn market ended the week with some selling, but didn’t lose much ground. We’ll know quite a bit more about how the trade sees this corn crop after this coming Friday’s USDA report. Keep some flex with your plan.

SOYBEANS

Beans had a poor week, with selling coming in for much of the trading sessions. On Friday, November beans settled down 6 at $10.27. This was 10 ¼ off the high and 1 ¼ off the low. Beans lost 27 ½ cents on the week. October meal settled 2.9 lower on the week at 280.5, while soy oil ended the week at 50.81 down 0.89. The bean market saw the buyers back off even in the face of a 4% drop in crop conditions and a poor-performing weather system that came across the ECB. For our farm, we had an 80% chance of rain with most models calling for a half inch of rain, but we had a tenth. This bean situation remains one in which the US balance sheet looks to remain quite tight while the world stocks remain burdensome. If USDA slashes yield much, they’ll definitely have to cut demand as carry-out is already down at 290 mb. They have the ability to do so with our new-crop export program, pitiful as China remains on the sidelines.

DEMAND

Soybean exports were a net cancellation for old-crop of 24k tons, which was 160k less than we saw canceled a week ago. 818 kmt were posted for the next marketing year, so bean exports overall were down around 300k. Basis was widening for the most part.

- My local beans: 55 under November (15 cents wider)

- Decatur: 25 under November (a dime wider)

- River: 27 under November (a penny improved)

CASH SOYBEANS

Cash beans were losing ground once again. Heck, my local basis widening by 15 cents was salt in the wound for those looking to sell some fall beans. Given that harvest is upon us, we should expect wide basis levels, especially with the river being so stagnant. It’s not hard to imagine we’d see river levels so poor given a non-existent new-crop export book. To complicate things further, the Mississippi and Ohio rivers are getting low enough that we may see barges that can’t float down the river at capacity. It’s amazing how quickly that happened, but with such a dry August, it’s not hard to fathom. For this fall’s beans, I’d be looking to store a few if possible, especially if you can do it on the farm. Given big carry to the first of the year and even out to next summer, at-home storage could pay big dividends, especially with basis likely to improve from such wide levels currently.

2026 SOYBEANS

November 2026 beans settled at $10.70, down 13 on the week. I still caution people from getting too aggressive in planting a ton of beans without some sort of protection. If current prices and profit margins are what are making you feel confident in that position, I’d be doing something about those prices. Likely, Brazil will plant 2-3% more acres, while the US grower could plant 5 ma or more next spring. With a 17-million-acre gap for this year, I expect that to narrow substantially. Some have bought puts close to the market and sold $12 and above calls to lock in some worst-case scenarios. I like a strategy like that for those who are planting a good chunk of beans this coming year.

November ‘25 Soybean chart

As always, use the AgMarket.Net Profitability App to help you figure your break-evens and put your plan in place:

Let me know if I can help in any way. These markets are tricky, but with a plan in place, we can take the emotion out and make better decisions.